Blockchain is an emerging technology that could be revolutionary. It was originally invented for Bitcoin, the digital currency. But its potential is far wider, and many different industries are actively investigating the potential of using blockchain-based solutions.

I recently had the opportunity to sit down with Martha Bennett, Principal Analyst at Forrester Research, and explore the possibilities for corporate applications of blockchain as well as its limits. For those who weren’t able to attend the session, this article will provide a look into what we discussed.

What is Blockchain?

While blockchain is still extremely young, and we aren’t sure where it’s headed, people have begun to find potential corporate applications for the technology, such as tamper-evident records, real-time demand-supply matching, auditability, distributed operations, and more. Blockchain’s power lies in the fact that it allows digital information to be shared among network participants with a high degree of integrity assurance. But “blockchain” isn’t one single technology – it’s an architectural principle that has several defining characteristics:

-

Write once, append only

-

Cryptographically secured (but not by default encrypted!)

-

Distributed and wholly or partially replicated among network participants

-

In its pure form, decentralized

There are two main categories of blockchain: permissionless (think Bitcoin and Ethereum, where anyone can participate and there’s no vetting) and permissioned (where participants are known and vetted, and rules apply on who can participate).

Blockchain is a genuine innovation, but it’s not a miracle cure. There are challenges and limitations, both in the technology itself as well as in the adoption of it.

Adoption Challenges

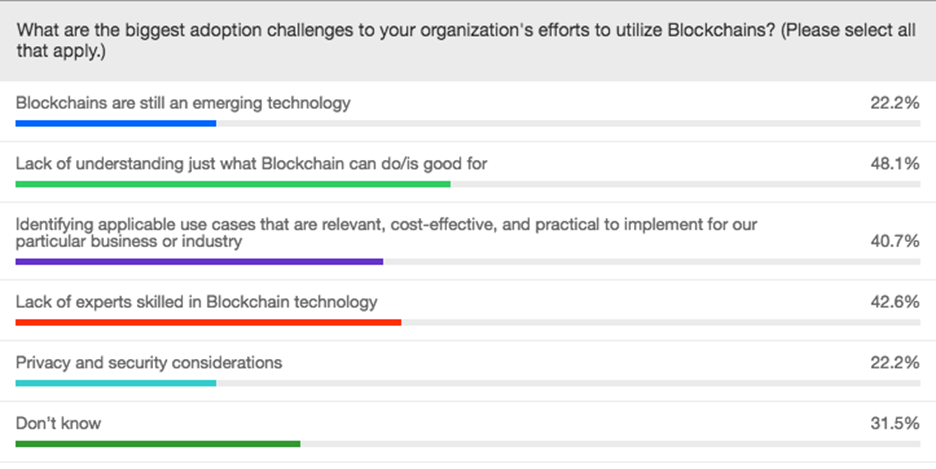

The adoption challenges that the webinar attendees reported in our poll are in line with what Forrester is seeing overall. As you can see by the poll conducted in our webinar, 48% of the audience selected a lack of understanding around exactly what blockchain is to be a main deterrent for adoption and 42% said a need for skilled experts to apply the technology is an issue.

Blockchain Myths

Blockchain is still very new, so all the typical challenges associated with emerging technology apply to the application of it. Many people still aren’t sure what it can be used for, and if they do have ideas for use cases, they aren’t sure if it will be cost effective or practical to implement. The lack of experts is a significant deterrent as well — implementation requires knowledge of cryptography, advanced math, database design, consensus algorithms, P2P networking, and distributed computing, to mention just a few. Privacy and security concerns are ever-present as well. These gaps in information and expertise often skew reality and breed myths as speculation about the future of a technology ensues.

Here are 3 myths about blockchain that were debunked during the webinar:

Myth 1: Smart Contracts Provide Legal Protection

There’s a notion that “code is law” with these new transactional platforms. The idea is that you can avoid intermediaries by using self-executing contracts — for example, if a service isn’t delivered as promised, an automatic refund is issued. That’s fine in theory. In practice, it’s a different story. First of all, the law is still the law.

Secondly, smart contracts are no more and no less than business rules encoded in software. But they are only as good as the person who devised the rules and the programmer who translated them into code. Smart contracts are NOT contracts in a legal sense unless a separate contractual agreement exists.

Myth 2: Transparency Is Always Good

One of the main attractions of blockchain is the level of transparency inherent in it. But transparency isn’t always appropriate or legal. For example, privacy and data protection laws dictate that not everyone should be able to see all the data. Personal security concerns (such as exposing the physical address of someone who has just purchased a valuable item) trump transparency. Commercial confidentiality and antitrust considerations also have to be taken into account. For these reasons, blockchain-inspired solutions, rather than pure blockchain architectures, are being developed.

Myth 3: Data Cannot Be Altered Once Written

Complete guaranteed immutability technically isn’t possible. But it can be made prohibitively expensive (and economically unattractive) to tamper with a blockchain (for example, Bitcoin). History can indeed be rewritten — and sometimes needs to be rewritten, due to errors, fraud, bugs, etc. It’s important to note that existing solutions aren’t always technically viable, and sometimes a record will need to be removed from the chain.

Blockchain Has Some Growing Up to Do

Blockchain is still in the very early stages of development. Many people compare blockchain’s maturity today to where the Internet was in the early 90s. But actually, it’s not even that far along — we don’t have the equivalent of HTTP; we have no standards yet. Because of this – any many other issues, both technical and non-technical large-scale blockchain adoption isn’t imminent.

But the potential is to develop new business and trust models exists, and we’re now in the rational assessment stage. We’re seeing projects transition beyond proof-of-concept, but they are not yet proper blockchain networks with all ecosystem participants actually running nodes. Also, it’s important to note that, as mentioned earlier, many of the implementations are not pure blockchain architectures, but rather blockchain-based or blockchain-inspired.

The Use Case Comes First

We have to remember not to lead with technology. We always need to start with the use case. What problems do we need to solve? What opportunity are we trying to capture? We also need to consider why the problem hasn’t already been solved with some other technology. There may be a good reason, such as a problem with our operational processes — using a different technology won’t address these problems.

When to Consider a Blockchain-Based Solution

If you’re analyzing whether to pursue a blockchain-based solution, ask yourself the following questions:

-

Do multiple parties need access to the same data?

-

Do multiple parties need to write to the data store?

-

Do all parties need assurance that the data is valid and hasn’t been tampered with?

-

Do you rely on a costly intermediary or a complex, unreliable process to reconcile the transactions of multiple parties? Or is there no system available today that does what you require?

-

Are there good reasons not to have a centralized system?

If the answer to these questions is “yes,” then it’s worth continuing to explore a blockchain-based solution. Just keep in mind Amara’s Law: “We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.” It’s smart to reimagine your industry and your company, but be sure to consider both how you’ll achieve the required network effect and all the implications down the road.